Submitted by: Dominick Harnett

Abstract

The Iran Nuclear deal, formally the Joint Comprehensive Plan of Action (JCPOA), was a framework negotiated between the P5+1 (UN security council members + Germany and the European Union) and Iran in order to curb Iran’s ability to build nuclear weapons in exchange for lifting sanctions related to the Iranian nuclear program. Sanctions put on Iran over the years have stifled its economy. The JCPOA lifts many of these sanctions which opens up vital financial revenue streams for banking and other loans. What this paper will explore is: Has the JCPOA had a real effect on the Iranian Economy since its signing in 2015? The Iranian Economy has grown over the last two years. I intend to show if the JCPOA has had a direct effect on the GDP growth and how significant the effect is.

By showing how much of an effect the JCPOA has had on the Iranian economy so far is important because it will reveal just how motivated the Iranians are to keep the agreement going. President Trump recently gave a speech in October 2017 decertifying the agreement and now is leaving it up to congress to make changes to the agreement. Iran wants to stick to the original agreement, but they may be willing to renegotiate some terms of the agreement if the JCPOA has had a large positive effect on their economy. Therefore giving Iran a much stronger appeal to keep the deal going and this will give the US more negotiating power to change some of the terms of the deal.

I will approach this research paper by accessing as many records I can on the Iranian economy. Things such as: The GDP Growth; the size of the sectors of the economy; the changes in these sectors because of the JCPOA; the direct and indirect economic impact of this change. I will also access data from WORLDBANK and the IMF which have great data on the economy of Iran. The IMF regularly puts out press releases about the economy in Iran and how the JCPOA may be impacting their economy.

Many experts say around 20% of the economy of Iran is affected by the sanctions related to the JCPOA. Lifting these sanctions theoretically will have a positive effect, but a majority of the economy will have little direct impact from the lifting of these sanctions. Things such as corruption and mismanagement may have a bigger role. But what I intend to show is that the deal is having a significant enough impact that will put enough pressure on Iranian politicians to work with the United States.

The Economic Impact of the JCPOA on Iran

The Joint Comprehensive Plan of Action (JCPOA) was announced on July 14, 2015. The countries involved in the JCPOA sought to achieve from the deal an Iran free of nuclear weapons as well as attempting to integrate Iran into the global community. Iran sought to lift the sanctions related to its nuclear program in the hopes it would grow its economy. The question that will be attempted at answering in this paper is : What has been the economic impact of the JCPOA on the Iranian economy since its implementation?

Framework of the JCPOA

The framework of the deal is designed to restrict Iran’s ability to build a nuclear weapon. The Obama administration’s goal during negotiations was to increase the time it would take Iran to build a nuclear weapon to at least one year up from just a few weeks. The term used for the amount of time it would take for a country to develop a nuclear weapon given all its available resources is known as the “breakout time”. Prior to the agreement the Obama Administration believed that Iran’s breakout time was just a few weeks. To make this happen the JCPOA restricts uranium enrichment done at the Fordow and Natanz enrichment plants to just 5%. To build a nuclear weapons requires around 80%.[1] It also requires that the heavy-water reactor at Arak be shut down. Heavy-water creates a plutonium by-product that can be used to create weapons-grade material. The deal also limits the variety of centrifuges that Iran can use to enrich its uranium. There is also a high degree of oversight over these nuclear sights through the International Atomic Energy Agency (IAEA). This is the group in charge of inspections in making sure Iran fulfills their end of the deal.

It is worth noting that many of these restrictions on the low percent of enriched uranium as well as the amount of centrifuges Iran can have do eventually expire. Centrifuge restrictions will be lifted after 10 years and the limits on enriched uranium will be lifted after 15 years.

If Iran maintains the standards put forth in the JCPOA then it was agreed upon by the P5+1 that all sanctions related to Iran’s nuclear Program would be lifted. These include all unilateral sanctions imposed separately by the EU or the United States as well as UN sanctions. These sanctions were lifted between 4 to 12 months after the implementation of the accord as Iran was in compliance of the deal via the inspections of the IAEA.

Economy of Iran Prior to the JCPOA

Iran has a well diversified economy compared to many other countries in the MENA region. Iran is a major oil producer in the world, but the oil industry makes up just 23% of its GDP.[2] Most of its economy, around 50%, comes from the service industry which has allowed Iran to be somewhat resilient to many of the sanctions that were being placed on Iran. Manufacturing and precious metals mining make up another 20% of the GDP. The Economy in Iran from 2013-2015 had been seeing low to negative economic growth. Sanctions placed on Iran limiting exports of oil and precious metals caused the Iranian economy to take a hit. There was also high inflation during this time as well as the Iranian Rial’s value dropped to nearly half of its worth compared to the USD in 2013. In 2013 the Ministry of Petroleum said that the government was losing between $4-8 billion in losses each month due to these sanctions.[3] Iran had already been moving to a more self-reliant economy, but the new round of sanctions implemented by the US and EU in 2012 took a significant effect on Iran’s economy which reliant on international markets and this caused the economy of Iran for the few prior years before the JCPOA to stagnate or deflate.

Oil and the economy in Iran

Oil is a large part of the economy in Iran. While much of the other sectors in Iran are seeming to head towards the private sector the oil sector remains very much in control of the state. The constitution prohibits private ownership of any oil production. Oil production in Iran is under the control of the National Iranian Oil Company (NIOC). Much of Iran’s oil production is using old and dated equipment[4]. There was little incentive to improve the technology in oil production because of the heavy subsidies and the natural tendency of state-owned enterprises to be inefficient. The 5-year economic plan from 2011-2016 called for the upgrading of much of the oil production technology being used in Iran. However, because of the scale and age of much of the fields, it required more investment than was allocated during that period to fully upgrade the equipment. But much of this is changing within the last 2 years. Prior to the signing of the Iran Nuclear deal in 2015, 64% of the oil produced in Iran was used by Iranians[5]. With the signing of the deal Iran is now able to export far more oil to international markets as sanctions are lifted. This has allowed Iran to reduce subsidies on oil to its own population and use the extra money to quickly upgrade the technology used in oil production increasing their efficiency.

Inflation in Iran has been at high levels over the last several years. In 2013, the annual inflation rate was at 40%.[6] The Iranian rial has seen deflation over the past few years directly related to the artificially low demand for Iran’s oil.

Iran’s economy is bogged down by a huge bureaucracy and the deep roots of bonyads and other entities like the Iranian Revolutionary Guard Corps (IRGC). This has dissuaded many foreign banks and entities from investing in Iran, irregardless of sanctions. The economy of Iran has seen significant liberalization under President Rouhani, but a large part is still in the public sector.

Sanctions

The first round of sanctions were placed on Iran following the 1979 revolution. Another round of sanctions were imposed by the United Nations in 2006 to try and halt Iran’s Uranium Enrichment program. In 2012, the United States along with the EU and UN introduced an oil embargo on Iran as well as barring financial transactions with Iranian entities. Iran has struggled to keep their Oil and gas production technologies updated due to these sanctions which has led to significant inefficiencies. In addition to sanctions restricting Iran’s ability to find markets for its oil, Iran has also lost revenue in their attempts at repatriating oil income. Iran was barred from using many international banking and financial systems which has forced them to find other more expensive means in order to get payments. Iran has also been unable to update many of their airplanes and other means of transporting cargo causing even more inefficiencies.

In March of 2012 Iran was barred from using SWIFT, an international banking network that allowed for the cross-national transactions of money. SWIFT is based in Belgium, and in 2012, in a response to Iran’s nuclear program, the United States and EU issued sanctions which excluded Iranian banks from using SWIFT. Iranian banks were no longer able to transmit payments or letters of credit, deeply damaging Iran’s ability to conduct foreign trade and transfer money. With the Implementation of the JCPOA Iranian banks were again allowed to access SWIFT.

Iranian banks that had assets and branches in Europe were reopened following Implementation Day. Iran would also be allowed to participate again in financial insurance markets. Iran had been denied access to financial insurance which dramatically increased their risk of losing valuable capital should a financial interaction with a foreign entity fall through. The United States still bars US companies and banks from working with Iran with some exceptions.

Iran was barred from exporting oil to EU and US markets. Many worried that this would cause oil prices to go up since Iran holds 12.9% of known global oil reserves.[7] This was not the case because of a fracking boom at around the same time happening in the United States. This oil embargo caused Iranian oil exports to drop from 2.2 million barrels per day in 2011 to just 700,000 in 2013.[8]

Iran was denied access to EU airports with their cargo flights. This forced Iranian exports of other goods to take other longer routes increasing costs. They also could no export precious metals such as gold and diamonds.

It was agreed upon that all EU non-nuclear related sanctions against several Iranian companies, people, and organizations, such as the IRGC, would be lifted after 8 years. US non-nuclear related sanctions were not part of the deal. This is significant because US sanctions on Iran often apply worldwide, EU sanctions only relate to Europe.

After the first report by the IAEA came back and confirmed Iran’s compliance, Iran was then allowed access to around $100 billion in frozen assets overseas. This was the estimate established by the U.S. Treasury department. Many of these assets were from the sale of Iranian oil, but the money often got stuck in overseas bank accounts and were not accessible by Iran due to the sanctions. According to Mark Dubowitz, director of the Foundation for Defense of Democracies, the money was sitting in places like India, China, Japan, South Korea, and Turkey.[9] All these countries were major purchasers of Iranian oil during during the years of sanctions.

No new nuclear-related sanctions would be implemented as part of the deal. However, if Iran was ever found in violation of the agreement than all sanctions would “snapback” into place.

Many non-nuclear related sanctions still remain. The United States still maintains sanctions the barr US financial institutions and companies from doing business with Iranian businesses and its government. These were imposed after the 1979 revolution. This includes subsidiaries in other countries. Non-US companies that may wish to do business with Iran still cannot access U.S. dollar clearing houses making it extremely difficult to exchange money. These businesses cannot use U.S. dollars to buy or sell to Iran, their accounts cannot be in U.S. dollars. Transactions have been in other currencies such as Korean Won, or Indian Rupee[10], but it has been difficult for companies wanting to exchange these currencies without being able to exchange them for U.S. dollars first. There are also many specific individuals and entities that US and EU companies still cannot do transactions with. These are related to Iran’s weapons program as well as human rights violations.

Financial institutions that do do business with Iran are asked to scrutinize any money going in and out of their accounts with Iranian entities. This is because in 2007 the Financial Action Task Force (FATF) put Iran on a list of possible financiers of terrorism.[11] This has made difficult Iran’s efforts to bring money into their country.

A big remaining problem is the complexity of doing business with Iran while complying with these remaining sanctions. The United States, EU, and the UN all have varying sanctions that do not align. This raises challenges to businesses and financial institutions in the US and EU. In addition to this is that many US states have imposed sanctions on their own on doing business with Iran. Two-thirds of the states have imposed their own sanctions on Iran beyond the federal level[12].

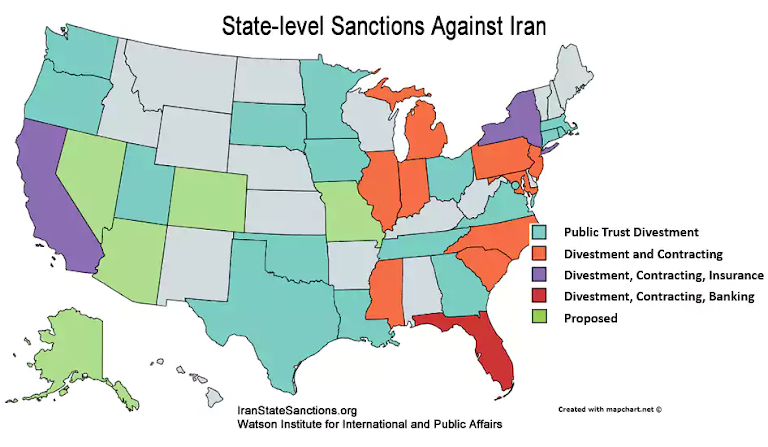

According to the Washington Post, many of these state-level sanctions are pegged to the US federal government’s list of state sponsors of terrorism and the lifting of US federal-level sanctions. But for a number of states it is left up to the individual states legislature with a variety of rules regarding the lifting of sanctions.

Lifting of Sanctions

Sanctions were lifted on January 16, 2016, this was known as Implementation Day. This came after the first reports by the IAEA confirmed Iran’s compliance. Iran’s export economy came roaring back in 2016 with the rollback of these sanctions. Oil production and exports rose significantly. But other domestic markets still remain depressed. Unemployment remains high in Iran as FDI (foreign direct investment) remains low. This is due to other non-nuclear related sanctions still in place as well as uncertainty among investors around the full implementation of the deal and the United States tentative status.

Iran’s total economy grew at a rate of 13.4% in 2016.[14] Just one year earlier, in 2015, Iran’s economy had seen a contractions of 1.3%. A large contributor to this change was in oil and gas exports. Oil and gas production is up over 60% which has contributed to 4.3% in economic growth.[15] Non-oil related industries grew at a slower rate of just 3.3%. This is higher than previous years, but still far lower than the increases in the oil and gas industries.

Investment contracted in 2016, despite the lifting of sanctions and opening to foreign investment. Again, this can be attributed to many financial firms having uncertainty of the legality of doing business with Iran as well as some continued US sanctions.

Unemployment actually increased in the past year from 12.4% at the end of 2016 to 12.6% in early 2017. This is despite the overall economy growing. This means that the largest growth in the economy, in the oil and gas sector, has not been creating as many jobs as expected. Like many other countries in the MENA region, Iran has a large number of young citizens under the age of 30. The government of Iran has put a lot of resources into educating this young population, but the economy and number of jobs available has been unable to keep up with the pace of population growth.

With the increase of oil and gas exports has been a stabilization of the Iranian Rial. Inflation is no longer at levels of 40% as seen in 2013. It is down significantly. By the end of 2016 inflation was down to below 10%. An impressive drop.[16]

The sanction relief has resulted in reintegrating Iran’s financial institutions with smaller non-US banks. According to the CBI (Central Bank of Iran), 238 small international banks have opened relationships with Iranian banks. This is an increase of just 50 post-2012 sanctions. (633 were before 2012 sanctions). This means a $12.8 million increase in credit has been opened to Iranian banks.[17] But many larger foreign banks have lacked in investment with Iranian banks. This makes it difficult to fund any large-scale operations without the large capital often required from larger banks.

The CBI and 15 other non sanctioned Iranian banks have been regiven access to SWIFT. This has allowed these banks to retrieve money that was frozen offshore and make other cross-national transactions. This is very important because of Iran’s large oil exports. Much of the money from the sale of oil and gas had to be either laundered, or was often just stuck frozen overseas in foreign accounts, unable to transfer to Iranian banks.

Some encouraging transactions that have been able to take place since Implementation day have been a 5 Billion Euro deal with an Italian company to rebuild Iran’s railway system. This is important because Iran’s infrastructure is aging and badly in need of upgrading. Prior to sanctions foreign companies were barred from sharing some technologies with Iran leading to Iran’s aged infrastructure. There is also a $4.8 billion deal currently in preliminary talks with the National Iranian Oil Company and a group of European companies to develop the South Pars gas field, this is an island just off the coast of southern Iran.[18] Also, French car companies, Renault and Peugeot, have begun to manufacture and sell their products in Iran. Airbus recently signed an $18 billion deal with Iran.[19]

A very interesting deal that was made is an $16.6 billion deal between Boeing and Iran air.[20] Boeing plans to sell 80 passenger jets to Iran Air, which had been using jets that date back to before the 1979 revolution. Boeing was allowed to go forward with this deal despite continued sanctions by the United States. There have been several attempts in congress to block this deal. Boeing released a statement that read, “We continue to follow the U.S. government’s lead in all our dealings with approved Iranian airlines and will remain in close touch with U.S. regulators for additional guidance.” Even with sanctions, money still talks.

Economic Outlook of Iran

In the short term Iran’s economy is expected to continue to grow. Oil exports will continue to flow as Iran tries to make up for lost time during the oil embargo. Growth in 2018-19 is expected to surpass 2017 growth. Investment is expected to increase despite some uncertainties. President Rouhani is seen as a moderating force that may ease foreign investors. He was just re-elected in May 2017.

Iran has also seen its trade deficit gap close up as oil exports increase. This has dramatically decreased the rate of inflation from 40% in 2013, to under 10% in 2016. Price shocks are now less common, creating a level of stability that is good for both Iranian producers and consumers.

Unemployment is predicted to remain at high levels of over 12% over the next few years. Domestic policy makers in Iran have called for the investment into non-oil related field to boost growth in those sectors. Policymakers hope this will spur job growth in fields that demand a higher education. Many of those unemployed are young men. The CBI has already redirected credit into non-oil related sectors.[21]

Remaining Obstacles for Iran’s economy

The sanctions relief given through the JCPOA has boosted Iran’s economy through access to financial markets as well as lifting the oil embargo, but hurdles still remain. Iran’s economy has not grown at the levels promised by President Rouhani. This has lead to Iranian officials criticizing the United States for not being faithful to the deal. It had also brought some political uncertainty to President Rouhani’s reelection campaign, but he was still able to win reelection in May 2017 showing that the Iranian people understand that some economic policies take longer to feel the impact.

Corruption and mismanagement of the economy remain hindering factors on the economy. As stated earlier in this essay, it is estimated that only about 20% of the economy is directly affected by sanctions. So any lack of growth must also be attributed to other sectors of the economy. Iran’s economy is over 50% run by the public sector. Many of the industries in this sector are bogged by huge bureaucracies, internal corruption and inefficiency. The aging infrastructure is also badly in need of updating. This is something Iran has attempted to bring up to speed over the last year. However, it will take years to make up for decades of lost time.

Unemployment remains high in Iran and is expected to remain that way over the next few years. Sanctions relief does not seem to be having an effect on creating new jobs in Iran. Much of the economic benefits from the JCPOA has been lopsided and gone mostly to the oil, gas, and financial industries.

Some onlookers worry about the increasing deficits in Iran’s budget. Since Implementation day Iran has seen deficits skyrocket. This is attributed to the government’s effort to make up for lost time by building and updating old infrastructure.

It’s also clear that revenue from Iranian oil isn’t as high as it could be. The price per barrel as of December 2017 is $57. This is down from prices above $100 per barrel in 2012-14. During those years Iran was under an oil embargo, therefore lots of potential revenue was lost. Iran has agreed to cap its oil output to 3.8 million a day for the 2nd half of 2017[22], as long as other OPEC members also agree to cap their output levels. It is unclear though that this has had a real effect on global oil prices.

One industry that has been doing well is law firms.[23] Companies looking to do business in the newly opened Iranian economy want to know how to comply with still remaining sanctions. There are some serious legal hurdles and compliances that companies must follow. There is still a fear of being hit by fines for violating other sanctions. Things are not clear-cut so companies have been seeking help navigating these hurdles.

Another hurdle to Iran’s economy is state-level sanctions that remain in the United States. Two-thirds of states in the U.S. have implemented their own sanctions regarding Iran.[24] This has hindered deals with Iran that were made legal at the federal level.

The Obama Administration State Department had sent letters to the governors of each of these states encouraging them to change their policies in regard to Iran[25]. They argued that the concerns of the individual states are the same concerns of the Federal government and therefore were being addressed in the JCPOA and were not needed at the state level.

These state-level sanctions do not technically violate the JCPOA, but they do complicate its implementation. All that is required in the JCPOA is that the US federal government “actively encourage” states to acknowledge the JCPOA. These state level sanctions have hindered to some degree expected economic recovery in Iran.

Perhaps the biggest obstacle to Iran’s economic outlook is the lack of FDI (Foreign direct investment) into Iran. Most of this is due to uncertainty with the JCPOA for a number of reasons. Non-US international banks have to take into account the possibility that Iran does not fulfill its obligations laid out in the JCPOA. This would cause a “snapback” of previous sanctions. There is also uncertainty of new sanctions being implemented for reasons unrelated to the Nuclear Program. Already new sanctions have been placed on Iran by the United States relating to the IRGC and Iran’s testing of ballistic missiles.[26]

Still, many of these uncertainties come from the United States under President Trump. Trump on the campaign trail often criticized the Iran Nuclear Deal calling it, “the worst deal he’s ever seen”. He has promised to pull out of the deal, but so far he has signed the recertification, continuing the JCPOA. However, more recently in October 13th, President Trump ordered the State department to label the IRGC as a sponsor of terrorism. The IRGC is deeply involved in many sectors of the economy which is sure to have a negative effect on it. This level of uncertainty with the US and the possibility of US withdrawal from the JCPOA has deterred many investors from doing business in Iran, particularly those that have assets in the US market. The impact created by the uncertainty of President Trump’s certification can even be seen in the value of the Iranian Rial. Already the Iranian Rial has depreciated from IR 32,400:1 USD in January to IR 34,156: 1 USD. It has continued to fall since Trump last certified the deal, reluctantly so, in July of this year. The impact of this uncertainty is also shown in the decreases in GDP growth in Iran since President Trump took office. However, it is still at levels far higher than those before Implementation Day.

Even with this uncertainty, many companies are willing to circumvent any obstacles that may come up because to the potentially lucrative gains of being able to access Iranian markets. But companies with ties to the US have largely stayed away from such risks.[27]

Iran had hoped unde the JCPOA they could attract more FDI, but this has largely not been the case with US and EU banks. Instead they have had to look elsewhere, particularly state-run financial institutions in places like Russia and China.

Conclusion

The JCPOA was signed by Iran in hopes that it would greatly boost their economy. While certain sectors of the economy have dramatically increased, such as oil and gas, much of the economy still struggles to see significant growth. Unemployment remains high as gains in the economy are lopsided toward oil, gas, and financial sectors. These areas which were directly affected by sanctions have not created many new jobs.

The sanctions relief under the JCPOA has not been as effective as Iran had hoped. FDI remains low as EU and US financial institutions still avoid investing in Iran as uncertainty with the JCPOA remain. Large financial institutions tend to be conservative with their investments and there is just far too much risk still with Iran. What if Iran is found to be breaking their obligations of the JCPOA and a snapback of sanctions occurs? What is the risk of being fined by the US for working with a sanctioned entity? Even if a company of financial investor wishes to do business in Iran, all the rules in place to legally complying with the rules greatly increase the administrative cost. For some companies and financial institutions this administrative cost will deter business and investments.

President Trump has said in a speech in October that he is decertifying the JCPOA and will leave it up to congress to decide which sanctions to place. The other countries in the P5+1 have said that they will continue to implement the agreement as long as Iran is found in compliance, but many EU banks have assets in the US and will not want to risk those. Business and investment must weigh the benefits and risk, and right now the risk is still very high for some.

Iran has improved its trade deficit with the increase in oil exports, but oil is not at the same prices as they were under Iran’s oil embargo from 2012-2014. Iran is struggling to make up for lost revenue and time.

What appears to be having the largest impact on the economic growth of Iran is its own domestic policies. Iran’s economy has become very self reliant over the last decades so much of its economic growth has to be attributed to its domestic policies. Corruption, inefficiencies of the public sector, mismanagement, aging infrastructure, and others have hindered economic growth in Iran.

However, Iran’s economy has grown since Implementation Day, and at least 25% of that growth can be contributed to sanctions relief. The oil embargo was having a huge effect on Iran. Iran went from 700,000 barrels a day during the oil embargo to almost 4 million barrels a day in early 2017. While FDI is not reaching levels that were expected, it has still increased, and continues to increase despite uncertainty.

But many believe that the true economic impact from new policies and agreements will take time to come to fruition. This sentiment is what got President Rouhani reelected despite criticism that the JCPOA was not working as he had promised. It’s true it takes time for the economic impact of policies to be felt. It is also true that old sentiments of distrust and uncertainties also take time to fade away. Perhaps in several more years, if things remain stable, companies will be more willing to navigate through any risks and uncertainties that may still be lingering. Iran has a lot to gain opening up to the global markets. As it becomes more open, it also has a lot more to lose.

References

Reuter’s Staff. (2016, February 17). Iranian Banks Reconnected to SWIFT Network After Four-Year Hiatus. Retrieved December 16, 2017, from https://www.reuters.com/article/us-iran-banks-swift/iranian-banks-reconnected-to-swift-network-after-four-year-hiatus-idUSKCN0VQ1FD

The Economist Staff. (2017, October 20). Uncertainty Over Nuclear Deal to Weigh On the Economy. Retrieved December 16, 2017, from http://country.eiu.com/article.aspx?articleid=1306005114&Country=Iran&topic=Economy

The Economist Staff. (2017, May 26). Another Challenging Four Year Ahead For Iran’s Economy. Retrieved December 16, 2017, from http://country.eiu.com/article.aspx?articleid=1825475566&Country=Iran&topic=Economy

World Bank Staff. (2017, October). Iran, Islamic Republic. World Bank Country Reports. Retrieved December 16, 2017, from http://pubdocs.worldbank.org/en/810181507054517387/MEM-Oct2017-Iran-ENG.pdf

Tradingeconomics.com. Iran GDP Annual Growth Rate. Retrieved December 16, 2017, from https://tradingeconomics.com/iran/gdp-growth-annual

Northam, Jackie. (2015, July 16). Lifting Sanction Will Release $100 billion To Iran. Then What?. NPR.org. Retrieved December 16, 2017, from https://www.npr.org/sections/parallels/2015/07/16/423562391/lifting-sanctions-will-release-100-billion-to-iran-then-what

OPEC Annual Statistical Bulletin. (2017). OPEC Share of World Crude Oil Reserves, 2016. OPEC Data/graphs. Retrieved December 16, 2017, from http://www.opec.org/opec_web/en/data_graphs/330.htm

Prepared By Olivier Basdevant, Selim Cakir, and Gaëlle Pierre (MCD), Aqib Aslam, Geerten Michielse, and Christopher J. Heady, (FAD), and Chady Adel El Khoury (LEG), Tohid Atashbar (Iran Parliament Research Center). (2017, February 10) Islamic Republic of Iran: Selected Issues. International Monetary Fund Country Report No. 17/63

Hart, Jo-anne, and Eckert, Sue. (2016, June 1). Most U.S. States Have Sanctions Against Iran. Here’s Why That’s a Problem. The Washington Post: Monkey Cage. Retrieved December 16, 2017, from https://www.washingtonpost.com/news/monkey-cage/wp/2016/06/01/most-u-s-states-have-sanctions-against-iran-heres-why-thats-a-problem-2/?utm_term=.dbc86b3d5edd

Laub, Zachary. (2017, October 13). The Impact of the Iran Nuclear Agreement. Council on Foreign Relations. Retrieved on December 16, 2017, from https://www.cfr.org/backgrounder/impact-iran-nuclear-agreement

International and Public Affairs at Brown University Staff. (2016). Iran State Sanctions Project. Watson Institute Security Project. Retrieved on December 16, 2017, from https://iranstatesanctions.org/portfolio/california/

Central Bank of Iran (2017) Retrieved on December 16, 2017, from http://www.cbi.ir/default_en.aspx

Reuters Staff. (2017, March 14). Iran to Keep Oil Cap at 3.8 Million Barrels a Day in Secondy Half 2017. Reuters #commodities. Retrieved on December 16, 2017, from https://www.reuters.com/article/us-iran-oil-opec/iran-to-keep-oil-cap-at-3-8-million-barrels-a-day-in-second-half-2017-idUSKBN16L1DT

World Bank Staff. (2017, April 1). The World Bank in Islamic Republic of Iran: Overview. The World Bank. Retrieved on December 16, 2017, from http://www.worldbank.org/en/country/iran/overview

Schweitzer, Andreas. (2017, January 17). Iranian Economy a Year After Sanctions. Financial Tribune. Retrieved December 16, 2017, from https://financialtribune.com/comment/419#comment-419

Euronews Staff. (2017, May 17). Iran’s Post-Sanction Economy Doing Well One Year After Nuclear Deal. Euronews. Retrieved December 16, 2017, from http://www.euronews.com/2017/05/17/iran-s-post-sanction-economy-doing-well-one-year-after-nuclear-deal

Daniels, Jeff. (2017, October 13). Boeing’s $8 Billion Deal on Sale of 80 Aircraft to Iran Aira Still Safe – at Least for Now. CNBC:Aerospace and Defense. Retrieved December 16, 2017, from https://www.cnbc.com/2017/10/13/boeings-8-billion-aircraft-sale-to-iran-air-still-safe-for-now.html

Cruid Oil Prices Today (2017) Oil:WTI. Business Insider: Markets Insider. Retrieved December 16, 2017, from http://markets.businessinsider.com/commodities/oil-price?type=wti

BBC Staff. (2015, March 30) Iran Nuclear Crisis: What are the Sanctions?. BBC News: Middle East. Retrieved December 16, 2017, from http://www.bbc.com/news/world-middle-east-15983302

[1] Council on Foreign Relations

[2] https://tradingeconomics.com/iran/gdp-growth-annual

[3] http://www.bbc.com/news/world-middle-east-15983302

[6] http://country.eiu.com/article.aspx?articleid=1825475566&Country=Iran&topic=Economy

[7] http://www.opec.org/opec_web/en/data_graphs/330.htm

[8] http://www.opec.org/opec_web/en/data_graphs/40.htm

[9]https://www.npr.org/sections/parallels/2015/07/16/423562391/lifting-sanctions-will-release-100-billion-to-iran-then-what

[10] IMF Economic Report On Islamic Republic of Iran February, 2017. Pp. 3

[11] IMF Economic Report On Islamic Republic of Iran February, 2017. Pp. 3

[12] https://www.washingtonpost.com/news/monkey-cage/wp/2016/06/01/most-u-s-states-have-sanctions-against-iran-heres-why-thats-a-problem-2/?utm_term=.dbc86b3d5edd

[13] https://iranstatesanctions.org/portfolio/california/

[14] http://www.worldbank.org/en/country/iran/publication/iran-economic-outlook-october-2017

[15] http://www.worldbank.org/en/country/iran/publication/iran-economic-outlook-october-2017

[16] http://country.eiu.com/article.aspx?articleid=1825475566&Country=Iran&topic=Economy

[17] http://www.cbi.ir/default_en.aspx

[18] https://financialtribune.com/articles/domestic-economy/57594/iranian-economy-a-year-after-sanctions

[19]http://www.euronews.com/2017/05/17/iran-s-post-sanction-economy-doing-well-one-year-after-nuclear-deal

[20] https://www.cnbc.com/2017/10/13/boeings-8-billion-aircraft-sale-to-iran-air-still-safe-for-now.html

[21] World Bank, Islamic Republic of Iran Economic Outlook Oct, 2017

[22] https://www.reuters.com/article/us-iran-oil-opec/iran-to-keep-oil-cap-at-3-8-million-barrels-a-day-in-second-half-2017-idUSKBN16L1DT

[23] https://financialtribune.com/articles/domestic-economy/57594/iranian-economy-a-year-after-sanctions

[24]https://www.washingtonpost.com/news/monkey-cage/wp/2016/06/01/most-u-s-states-have-sanctions-against-iran-heres-why-thats-a-problem-2/?utm_term=.dbc86b3d5edd

[25]https://www.washingtonpost.com/news/monkey-cage/wp/2016/06/01/most-u-s-states-have-sanctions-against-iran-heres-why-thats-a-problem-2/?utm_term=.dbc86b3d5edd

[26] IMF Report on Islamic Republic of Iran February, 2017

[27] http://country.eiu.com/article.aspx?articleid=1306005114&Country=Iran&topic=